PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex posted modest across-the-board gains for a second session amid strength in equities. Data showed Eurozone and UK consumer price inflation was positive and matched the expected pace last month. The FTSE 100 rose 0.4%, the CAC 40 climbed 0.4% higher, and the DAX strengthened 0.8%. In other news, the Bank of Canada made no changes to monetary policy settings, keeping rates at 0.25%, as expected. US data were a miss, as the NAHB Housing Market Index for this month was a surprise drop from last month's 86 print, to 83. President Biden was inaugurated today, and expected to sign a number of executive orders reversing energy policy from the previous administration. The President has also outlined a large stimulus package proposal. As of this writing, the Dow had gained 0.9%, the S&P 500 had climbed 1.4% higher, and the Nasdaq had rallied to 1.9% gains. The US dollar index was little changed, seeing see-saw trade about the unchanged mark today.

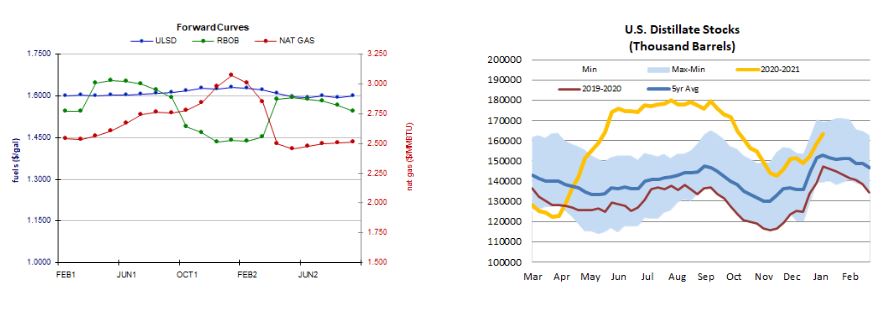

Forward Curves and Stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures continued lower today despite a slight uptick in the degree day forecast and tighter market balance expectation for next week. The Global Forecast System sees 421 HDDS over the next two weeks, up from 415 previously. This is below the 451-HDD 30-year average but tops last year's 400 HDDs during the same period. Also supportive, Refinitiv analysts raised their total US demand forecast for next week by 1.5bcf/d to 127.4bcf/d, while raising their supply forecast by just 0.10bcf/d to 99.8bcf/d, implying larger withdrawals from storage of 27.6bcf/d. The latest 1-5 day outlook from the ECMWF calls for mixed, near-normal temperatures in both the Midwest and Northeast. The 6-10 day outlook calls for above-normal temperatures in the Midwest and mixed but mostly below-normal temperatures in the Northeast. Cash natural gas prices well, with Henry Hub prices down 21 cents to $2.65mmBtu and Algonquin citygate prices falling from $5.28 to $4.50/mmBtu. Weekly natural gas and petroleum inventories from the EIA are delayed to Friday due to the holiday we had on Monday and the inauguration today.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures edged up in a thinly-traded upside session (higher high, higher low), consistent with our upside bias. Bullish momentum seems to be flagging, however, and slow stochastics and the RSI are bearish. Meanwhile, the MACD is bullish and the ADX strongly indicates an uptrend. We continue to see nearby resistance at the recent $1.6235 high, followed by $1.6424, whereas the 9-day ma ($1.5886) and then $1.5000 are seen offering nearby support. RBOB futures edged up today in an upside session, settling well off of the highs. Slow stochastics are bearish, while the RSI is hovering near the overbought line. Major averages point higher, but the MACD is neutral. We continue to eye $1.5756 and then $1.6000 for resistance, with18-day ma ($1.4693) and then $1.3899 support. We remain sided with the bulls for the moment, but as with HO we see flagging momentum. WTI futures also edged up in an upside session, settling well off of the highs. Technical indicators are similar to those in products. We remain neutral/bullish, seeing resistance at $53.93 and then at $55.58, with support expected at the 9-day ma ($52.62) and then at $50.54. Natural gas futures trade was also consistent with our directional bias, as futures fell in a downside session. We settled well off of the lows, however, printing a hammer-shaped candlestick that can precede a reversal. Slow stochastics and the RSI are not oversold yet, however, and so we'll stick to our guns for now, still seeing $2.403 and then $2.247 support, with resistance at the 100-day ma ($2.646) and then up at $2.769.