PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures again see-sawed about the unchanged mark today, settling mixed, with bullish US crude oil inventory data from the EIA supporting, whereas strength in the US dollar index and losses in global shares likely weighed. Following a disappointing GfK consumer climate survey in Germany, the DAX fell 1.8% today. The CAC 40 in France lost 1.2%, and the UK's FTSE 100 fell 1.3%. US durable goods orders for December were a miss, growing 0.2% against expectations for a 1.0% rise, although November orders growth was revised up by 0.3pp to 1.2% and December core capital goods orders growth of 0.6% beat the 0.4% forecast. The FOMC kept its Federal Funds target rate steady at 0-0.25% and made no changes to its monthly bond purchase program, consistent with market expectations. As of this writing, both the Nasdaq and Dow were down 1.2%, and the S&P 500 had lost 1.5%. Also unsupportive for crude, the US dollar index was up 0.5%.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures strengthened today along with the two-week degree day outlook and a tighter US market balance expectation for next week. Refinitiv analysts raised their total US demand forecast for next week by 2.8bcf/d to 126.6bcf/d, while trimming their supply forecast by 0.1bcf/d to 99.8bcf/d, implying larger withdrawals from storage of 26.8bcf/d (compared to 23.9bcf/d previously). The latest 1-5 day ECMWF outlook calls for mixed, near-normal temperatures in the Midwest but below-normal temperatures for most of the East Coast. The 6-10 day outlook, however, sees mixed and mostly above-normal temperatures for the eastern two-thirds of the country. For the next two weeks overall, the Global Forecast system sees 460 Heating Degree Days, up from 435 previously and topping both last year's 367 HDDs and also the 438-HDD 30-year average. Cash natural gas prices were mixed, as Henry Hub prices rose by 9 cents to $2.73/mmBtu and Transco Zone 6 prices in New York climbed 29 cents higher to $2.78/mmBtu, but as Algonquin citygate prices fell back 45 cents to $4.70/mmBtu. The EIA is due to release its weekly natural gas storage report tomorrow, expected to show a 136bcf withdrawal from storage for the week ended January 22 according to a Reuters poll of analysts. This would be well below last year's 170bcf withdrawal and also the 174bcf five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

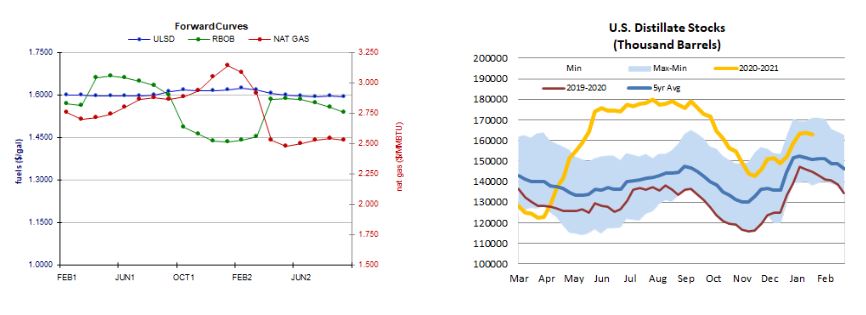

ULSD futures edged up 0.7% today in an outside session, as we saw both a higher high and a lower low, printing a star-shaped candlestick with very long wicks. As such, we remain on the sidelines, still looking to $1.6235 (recent high) and then to $1.6424 for resistance, whereas the 9-day ma ($1.5984, tested and held up today on a settlement basis) and then $1.5000 remain nearby support. RBOB futures, where we are neutral/bullish, slipped 0.2% lower - but in an upside session, hitting a fresh multi-month high of $1.5900 today. We'll maintain our neutral/bullish stance for now, but note that slow stochastics are entering overbought territory, confirming overbought conditions indicated by the RSI (71.2). Nearby resistance at today's $1.5900 high, followed by $1.6956, whereas the 18-day ma ($1.5184) and then $1.3899 should offer support. WTI added 0.5% today in an outside session, consistent with our neutral view which we maintain. We settled just north of the 9-day ma ($52.84) and so this becomes nearby support followed by $50.54, whereas $53.93 and then $55.58 are our nearby resistance levels. We sided with natural gas bulls yesterday, and were rewarded with 3.9% jump today in an upside session. We settled just under $2.769 resistance, and so we'll continue to keep an eye there and then up at $2.898, whereas the 100-day ma ($2.647) and then $2.403 are our nearby support levels. Slow stochastics and the RSI have plenty of headroom.