PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex once again saw see-saw trade about the unchanged mark today, settling mixed with support from strength in US and European shares and weakness in the US dollar index, whereas US-China tensions likely weighed on valuations. Asian shares fell overnight, particularly in Hong Kong and in Shanghai. European shares were mostly lower in the morning, but mostly recovered today. While the FTSE 100 fell 0.6%, the CAC 40 rose 0.9% and the DAX added 0.3%. US stock market indexes were seeing gains of over 1.8% as of this writing, despite a miss in fourth quarter US GDP growth. The world's largest economy grew 4.0% last quarter, below the 4.1% expectation, and contracted by 3.5% last year - the largest yearly contraction since 1946. Additionally, US new home sales for December were a miss at 842,000 (annualized rate), as consensus was up at 871,000. Other data were more favorable, however, as the US international trade in goods deficit for December was a narrower-than-expected $85.5bn, and weekly initial jobless claims fell to 847,000, beating expectations at 875,000. Also supportive for crude, the US dollar index was down 0.2% as of this writing.

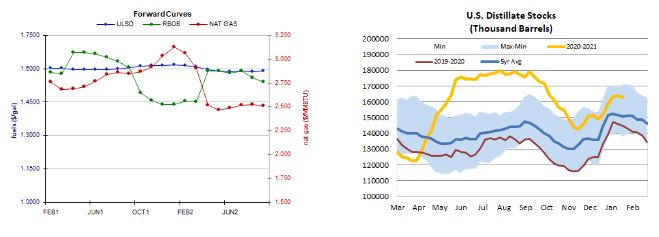

Forward curves and distillate stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures lost some ground today following a bearish weekly EIA storage report, despite a stronger two-week heating degree day forecast. The latest 1-5 day outlook based on the European model calls for near to above-normal temperatures in the Midwest but mostly below-normal temperatures on the East Coast. Next-day cash natural gas prices strengthened, with benchmark Henry Hub prices up 4 cents to $2.77/mmBtu, Transco Zone 6 prices in New York jumping $1.83 higher to $4.61/mmBtu, and volatile Algonquin citygate prices shooting up $5.05 to $9.75/mmBtu. The 6-10 day (EC) outlook sees above-normal temperatures across the eastern half of the country. For the next two weeks overall, the GFS sees 471 HDDs, up from 460 previously and exceeding both last year's 367 HDDs and the 436-HDD 30-year average. In bearish news today, the EIA reported a 128bcf withdrawal from storage for the week ended January 22. This was well below the 136bcf forecast, which was itself well below last year's 170bcf withdrawal and the 174bcf five-year average for the reporting week. Consequently, the surplus to last year increased to 2.8% and the surplus over the five-year average grew to 9.3%, with total storage levels now at 2.881tcf.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures edged down 0.4% today in an upside session, consistent with our neutral stance. We settled well off of the highs and near the bottom of the daily range, printing a shooting star. Major averages and the ADX still point higher, but other indicators are neutral, and neutral remains our stance. Bulls managed to hit a fresh multi-month high of $1.6311 and this becomes nearby resistance, followed by $1.6424, whereas the 9-day ma ($1.5968) and then $1.5000 remain nearby support. RBOB futures also hit a fresh multi-month high of $1.6119, and while we settled well off of the highs we still added 0.4%, consistent with our flat-to-higher price view, which we maintain. We note, however, that both the RSI and slow stochastics are overbought, and that the latter are threatening to cross for a sell signal. Meanwhile, candlesticks and major averages continue to point higher, while the MACD is natural. We remain neutral/bullish, seeing $1.6119 and then $1.6956 resistance, with 18-day ma ($1.5284) and then $1.4900 support. WTI fell 1.0% today but in an upside session, and we remain neutral. We settled back below the 9-day ma ($52.73) and this becomes nearby resistance followed by $53.93, whereas $50.54 and then $45.27 are our nearby support levels. Natural gas futures fell 1.4% today in a downside session, which was inconsistent with our upside bias. The RSI is in neutral territory, and the MACD and major averages are neutral as well. Slow stochastics point higher but are approaching overbought conditions. Still, we'll stick to our bullish guns for a session longer, still seeing $2.769 and then $2.898 resistance, with the 100-day ma ($2.649) and then $2.403 expected to offer support.