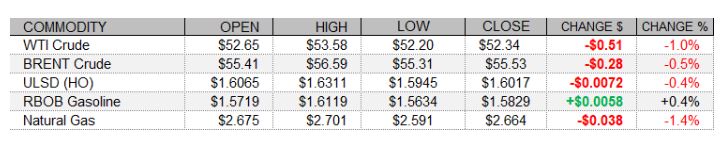

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex once again saw see-saw trade near the unchanged mark today, ending mostly lower, with mixed but generally supportive US and European economic data releases, but with fairly sharp declines in global equities likely weighing. Additionally, Baker Hughes reported another weekly rise in the US oil rig count. The count rose by 6 this week to 295, although this represents a drop of 380 from the same week last year. Despite encouraging French and German economic data releases, the CAC 40 dropped 2.0% lower today and the DAX fell 1.7%. The FTSE 100 in the UK lost 1.8%. The Canadian economy saw faster than expected growth of 0.7% in November, and US data were mixed but generally supportive as well. The University of Michigan consumer sentiment index saw a slight surprise downward revision from the preliminary estimate this month, falling to 79.0, and the NAR Pending Home Sales Index for December fell 0.3%, as expected, but the Chicago PMI for January saw a surprise rise to 63.8, US personal income growth of 0.6% last month far outpaced the 0.1% expectation, and the Core PCE rose 0.3% last month, above the 0.1% consensus forecast. Nevertheless, the major US stock market indexes were seeing losses of over two percent as of this writing. Johnson & Johnson's coronavirus vaccine was found to be 66% effective in preventing COVID-19 in large-scale global trial results.

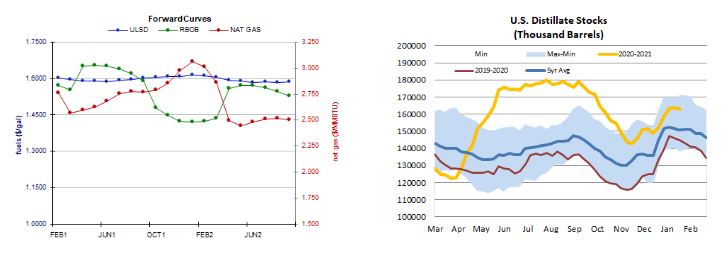

Forward curves for ULSD RBOB & NAT GAS along with Distillate Stocks

NATURAL GAS | WEATHER | INVENTORIES

NYMEX natural gas futures fell further today with a weaker degree day forecast and looser market balance expectation for next week, even as cash prices surged amid near-term cold in the Northeast. Transco Zone 6 prices at the New York citygate jumped $1.39 higher to $6.00/mmBtu, and already-strong Algonquin citygate prices shot up $1.75 to $11.50/mmBtu. Prices at Henry Hub shed one cent, to hit $2.76/mmBtu. Temperatures are expected to be well below normal in parts of the Northeast over the next five days, while the Midwest is expected to see above-normal temperatures, according to the latest EC outlook. The 6-10 day forecast calls for mixed temperatures in the Midwest but above-normal temperatures in the Northeast. For the next two weeks overall, the GFS cut its HDD forecast from 471 to 463 - still above last year's 367 HDDs and also the 434-HDD 30-year average. In supply-side news, Baker Hughes reported no change this week in the US natural gas rig count, holding at 88.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures edged down 0.1% today but in an upside session, as bulls took us for a trip north intraday to hit a fresh multi-month high of $1.6357. We came off and settled in the bottom portion of the daily range, printing another shooting star. We remain sidelined, given the mostly neutral technical picture and sideways trade in recent trading sessions. We see nearby resistance at today's $1.6357 high, followed closely by $1.6424, whereas the 9-day ma ($1.5977) and then $1.5000 remain nearby support. RBOB futures fell 0.7% today in an upside session. Slow stochastics have crossed for a sell signal in overbought territory, and the RSI confirmed overbought conditions. As with HO, however, we saw fresh high of $1.6293, which becomes nearby resistance, followed by $1.6956. We continue to see nearby support at the 18-day ma ($1.5394) and then down at $1.4900. We fall back to the sidelines. WTI futures shed 0.3% today in a downside session, with nearby 9-day ma resistance ($52.71) holding up on a settlement basis (followed by $53.93). We remain neutral, looking to $50.54 and then to $45.27 for support. Natural gas futures fell 3.8%, but in an outside session (higher high, but also a lower low). Still, with bears taking out nearby 100-day ma support ($2.648), we fall back to the sidelines. Next support at $2.403 and then at $2.247, whereas the 100-day ma and then $2.769 are seen offering resistance. Slow stochastics crossed bearishly but south of overbought territory; meanwhile, the RSI is neutral and so are the major averages.