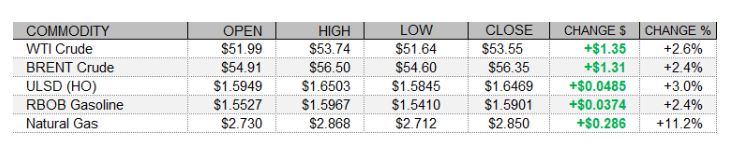

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex rallied along with equities today, following mixed but mostly encouraging economic data releases, despite strength in the US dollar. There was also a bullish note from Goldman Sachs. Eurozone and UK manufacturing data for last month were slightly stronger than expected, and Eurozone unemployment held steady at 8.3% in December as expected. The FTSE 100 closed 0.9% stronger, the CAC 40 gained 1.2%, and the DAX climbed 1.4% higher. US economic data releases today were mixed but mostly positive. The ISM Manufacturing Index fell from 60.5 to 58.7, short of consensus at 60.0 but still quite strong. The Markit Manufacturing PMI for last month was finalized at 59.2, beating the 58.0 expectation, and December construction growth of 1.0% in December topped the 0.8% forecast, even after an upward revision to November spending. As of this writing, the Dow was up 0.9%, the S&P 500 had gained 1.7%, and the Nasdaq was rallying 2.5%. Also supportive for crude was a note from Goldman Sachs saying $65/bbl Brent prices could be reached by July. Meanwhile, the US dollar index was up 0.4% as of this writing, which is unsupportive for crude.

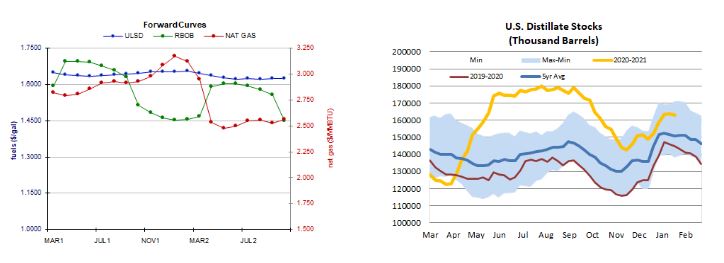

ulsd rbob and nat gas forward curves and distillate stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures rallied today with a stronger degree day forecast and a tighter view of the market balance this week. Refinitiv analysts raised their total US demand forecast for the current week by 3.1bcf/d to 128.4bcf/d, while adding just 0.20bcf/d to their total supply forecast - implying 28.5bcf/d withdrawals. The market is seen tightening further next week, with demand jumping 9.7bcf/d higher to 138.1bcf/d, while supply falls by 0.2 to 99.7bcf/d (suggesting 38.4bcf/d pulled from storage). For the next two weeks, the Global Forecast System sees 471 HDDs, up from 463 previously, and well above both the 436-HDD 30-year average, and last year's 388 HDDs. The latest 1-5 day ECMWF outlook calls for near to above-normal temperatures in the Midwest and Northeast, but the 6-10 day forecast is supportive as temperatures in the Northeast (except Maine) and the Midwest are seen 5-15 degrees Fahrenheit below normal.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX HO futures jumped 3.0% higher today in an outside session - hitting a lower low near the 9-day ma but rebounding and rallying to a fresh multi-month high of $1.6503. This becomes nearby resistance, followed by $1.7000. We remain neutral for now, given an overbought RSI, neutral slow stochastics and MACD. Nearby support remains at the 9-day ma ($1.6033) and then down at $1.5000. RBOB futures jumped 2.4% higher today but in a downside session, consistent with our neutral stance, which we maintain. Slow stochastics still look heavy, and the RSI remains overbought. Major averages point higher, but the MACD is neutral. We continue to see nearby resistance at Friday's $1.6293 high, followed by $1.6956, whereas the 18-day ma ($1.5474, tested and held on a settlement basis) and then $1.4900 are expected to offer nearby support. WTI futures, where we are neutral, climbed 2.6% higher in an outside session. We did not match the recent $53.93 high, which remains nearby resistance - followed by $55.58. Nearby support at the 9-day ma ($52.79), followed by $50.54. Finally, NYMEX natural gas bulls took us 11.2% higher today, after a wide gap higher over the weekend. Bulls took out $2.769 resistance, and this becomes nearby support, followed by the 100-day ma ($2.652). Stochastics point south, the RSI is neutral, as are major averages, and with a mixed technical picture we remain sidelined, awaiting further developments. We see resistance at $2.898 and then $3.171, whereas $2.758 and then $2.403 are seen offering support.