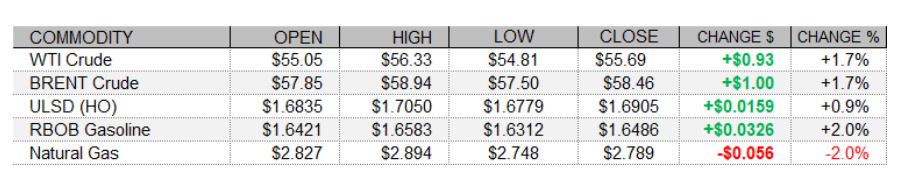

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures opened higher amid strength in global shares and following bullish crude oil stock data from the API, but turned lower later in the session, as EIA inventories proved to be neutral to unsupportive all around. See our DOE Report for details. Additionally, stock market indexes came off of their highs, with European shares settling mixed despite generally stronger than expected economic data releases including the final Eurozone Composite PMI and flash Eurozone HICP for last month. The FTSE 100 slipped 0.1% lower, the CAC 40 was little changed, while the DAX gained 0.7%. US data today were encouraging, as ADP reported a jump of 174,000 in private payrolls last month - well above expectations at 50,000. Additionally, December payrolls were revised up by 45,00. Also encouraging, the ISM Services Index for January came in at 58.7, up from an upwardly-revised 57.7 in December, beating consensus at 56.8, and indicating the expansion in the sector accelerated. US stock market indexes were seeing flat-to-higher trade as of this writing, with the Dow steady while the S&P 500 was up 0.3% and the Nasdaq had gained 0.4%. The US dollar index was flat. In supply-side news, the OPEC+ JMMC met today and made no recommendations to change policy.

NATURAL GAS | WEATHER | INVENTORIES

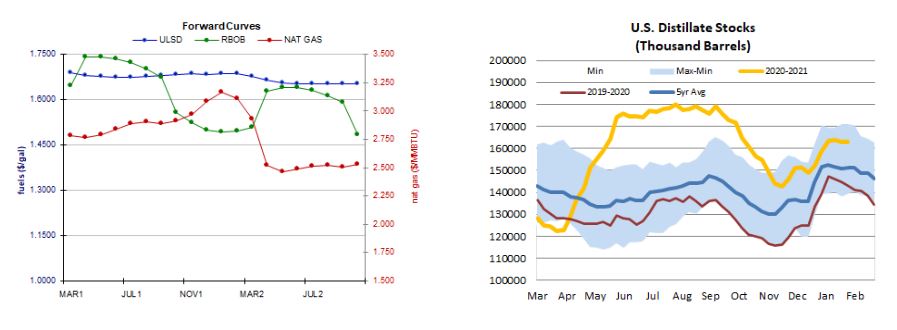

Natural gas futures on NYMEX continued lower today, as there were some unsupportive shifts in the outlook - even though colder than normal temperatures are still the expectation. The GFS sees 506 HDDs over the next two weeks, down slightly from 508 previously, but this is still well above the 30-year average of 421 and also last year's 388 HDDs. The latest 1-5 day ECMWF outlook calls for below-normal temperatures in the Midwest and for much of the East Coast - but above-normal temperatures are expected in the Northeast. The 6-10 day forecast is very supportive, with double-digit deviations below normal temperatures in degrees Fahrenheit expected across much of the country, including the Midwest and parts of the Northeast. Cash natural gas prices strengthened further, with Henry Hub prices up 36 cents to $3.24/mmBtu, Transco Zone 6 prices at the New York citygate up 55 cents to $5.46/mmBtu, and Algonquin citygate prices shotting up $4.15 to $12.50/mmBtu amid inclement weather. The EIA is due to release its weekly natural gas storage report tomorrow, and analysts polled by Reuters see a 192bcf withdrawal being reported. This would be well above last year's 155bcf withdrawal and also the 146bcf five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX ULSD futures gapped higher, consistent with our upside bias and hitting a fresh multi-month high of $1.7050 before coming off to settle in bottom portion of the daily range, printing a shooting star. The RSI is deeply overbought, and slow stochastics look set to confirm by entering overbought territory. On the other hand, the MACD has crossed bullishly and the ADX is rising as it indicates an uptrend. Most indicators remain bullish, and so will we, seeing resistance at today's $1.7050 high, followed by $1.7500, whereas the 9-day ma ($1.6211) and then $1.5000 remain nearby support. RBOB futures also gapped higher overnight, opening near the top of the prior session's range, and we closed up 2.0%. Today's candlestick looks like a Doji star, however. The RSI is overbought, but slow stochastics cannot confirm, and major averages point higher. We'll continue to favor the upside for now, seeing resistance at today's fresh high of $1.6583, followed by $1.6956, while the 18-day ma ($1.5642) and then $1.4900 are seen offering support. WTI futures also gapped higher overnight and hit fresh highs, closing off of those highs for a 1.7% gain. We remain bullish for now, seeing resistance at today's $56.33 high and then up at $59.67, with the 9-day ma ($53.23) and then $50.54 seen offering support. As with products, the RSI is overbought but slow stochastics have a little bit of headroom. Finally, NYMEX natural gas futures lost 2.0% in a downside session, but nearby $2.758 support held on a settlement basis, and $2.898 resistance held as well. These remain our nearby levels, followed by $2.403 below and $3.171 above, respectively. We remain neutral.