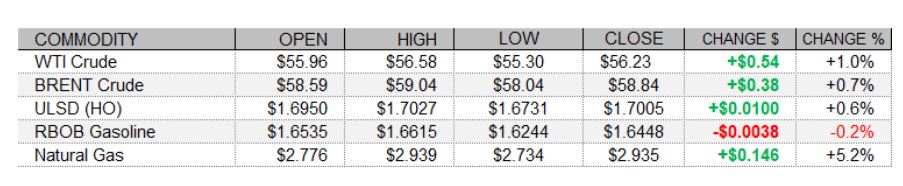

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex settled mostly higher today, with strength in European and US shares supporting, whereas a continued rally in the US dollar was unsupportive. The UK Construction PMI for January (49.2) was a miss, falling into contractionary territory unexpectedly. The Bank of England kept monetary policy settings unchanged. The FTSE 100 fell 0.1% today, but other European shares mostly strengthened following encouraging Eurozone retail sales data showing 2.0% growth in December and a shallower than previously estimated drop in sales the month prior. The CAC gained 0.8% and the DAX strengthened 0.9%. US data today were mixed. Fourth quarter US nonfarm productivity fell 4.8% year-on-year, worse than the 2.8% forecast - but third quarter productivity was revised up from a 4.6% to a 5.1% yearly growth rate. Also in the minus column was the Challenger Job-Cut Report showing an increase in planned layoffs to 79,552 last month. In positive news, factory orders growth of 1.1% in December beat expectations and November orders were revised up, and weekly initial jobless claims fell to a lower-than-predicted 779,000. As of this writing, the Dow, S&P 500, and Nasdaq were all up about one percent. While this was supportive, a jump in the US dollar index of 0.39% to levels not seen since December 1 was unsupportive.

NATURAL GAS | WEATHER | INVENTORIES

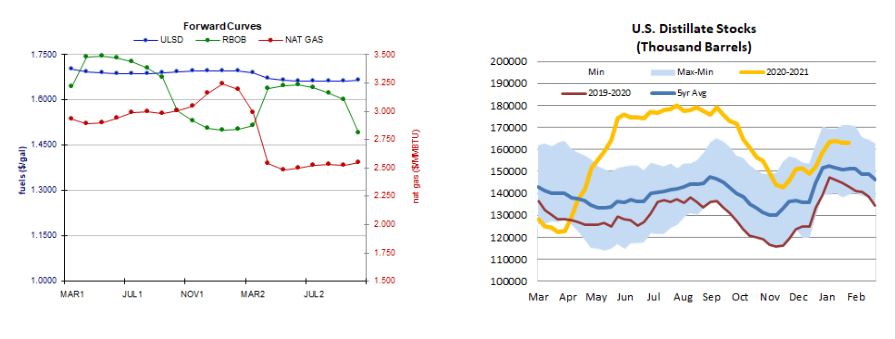

Natural gas futures strengthened today with an upgrade to the heating degree day forecast. The GFS raised its two-week HDD forecast by 23 to 529, which is well above the 30-year average of 418 and last years 388 HDDs. According to the European model, temperatures in the Midwest are expected to be well below normal over the next 5 days, and mostly below normal on the East Coast, except for some above-normal temperatures in the Northeast. The 6-10 day outlook is bullish, with temperatures seen falling to 15 degrees below normal in much of the Midwest, and below-normal temperatures are the expectation in the Northeast as well. Algonquin citygate cash prices jumped $1.72 higher to $14.22, but Transco Zone 6 prices in New York fell back $2.33 to $3.13/mmBtu and Henry Hub prices eased down 23 cents to $3.01/mmBtu. The EIA released its weekly natural gas storage report today, showing an as-expected withdrawal of 192bcf for the week ended January 29. Total storage levels fell to 2.689tcf, which is just 1.5% higher than last year but still 7.9% above the weekly five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures continued higher today, consistent with our directional bias. However, slow stochastics and the RSI are both now overbought, we printed a hammer-shaped candlestick, and we saw both a lower high and a lower low today, making it a downside session. Still, we'll await evidence that the trend has ended before abandoning the bulls. We see nearby resistance at $1.7050 and then $1.7500, with nearby support at the 9-day ma ($1.6350) and then down at $1.5000. RBOB futures hit a fresh high of $1.6615 but came off and settled down 0.2% - still in the upper half of the daily range. As such, and as slow stochastics cannot confirm the overbought conditions the RSI is indicating, we remain neutral/bullish. Nearby resistance at today's $1.6615 high, followed by $1.6956, whereas the 18-day ma ($1.5697) and then $1.4900 are seen offering support. We also favored the upside for WTI, and futures gained 1.0% in an upside session. Slow stochastics and the RSI are overbought, but we'll continue to favor the bulls for the moment. We see nearby resistance at today's $56.58 high, followed by $59.67, with 9-day ma ($53.67) and then $50.54 support. Natural gas futures gapped lower but then jumped 5.2% higher today in an outside session. Indicators remain mixed and mostly neutral, and we remain sidelined awaiting further developments, with support seen at $2.898 and then $3.171, whereas $2.898 and then $2.758 are now our nearby support levels.