PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures continued higher today amid supportive US economic data releases, losses in the US dollar index, and mostly higher trade in US equities, despite a bearish revision to the 2021 global oil demand forecast in the EIA's Short-Term Energy Outlook. The EIA released its February STEO today, in which the agency cut its 2021 global oil demand growth forecast by 180kb/d to 5.38mb/d, but raised its 2022 growth estimate by 190kb/d to 3.5mb/d. The EIA expects US crude oil production to fall from an estimated 11.0mb/d in January to 10.9mb/d in June, before it starts rising in the second half of the year. The agency bases its forecasts on IHS Markit estimates that US GDP will grow 3.8% this year and 4.2% in 2022, after a 3.6% drop last year. In US news, the Job Openings and Labor Turnover Survey (JOLTS) put openings at 6.646m in December, beating expectations at 6.400m and up from an upwardly-revised 6.572m in November. European shares closed mixed today with the FTSE 100 and the CAC 40 up 0.1%, while the DAX lost 0.3%. As of this writing, US stock market indexes were trading flat to higher with the S&P 500 down 0.1%, whereas the Dow and the Nasdaq were seeing gains of 0.1% and 0.2% respectively. The US dollar index was down 0.4%, which is supportive for crude oil prices.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures turned south today amid a weaker two-week heating degree day forecast and a looser US market balance expectation for next week. Refinitiv analysts now see total US demand of 148.4bcf/d outpacing US supply at 99.1bcf/d next week, implying smaller withdrawals of 49.3bcf/d (compared to yesterday’s forecast at 53.2bcf/d). The Global Forecast System cut its heating degree day forecast for the next two weeks from 544 to 521, which is still well above both the 30-year average of 402 and last year's 405 HDDs over the same period. In the cash market today, prices at the Henry Hub benchmark fell from $3.49 to $3.40/mmBtu, Algonquin citygate prices fell from $11.50 to $11.25/mmBtu, and Transco Zone 6 prices in New York dropped from $4.27 to $4.07/mmBtu. The latest 1-5 and 6-10 day outlooks (EC) call for below-normal temperatures in both the Midwest and the Northeast, with large deviations below normal seen in the former. According to a Reuters poll of analysts, estimates for the weekly EIA petroleum inventory report for the week ended February 5 call for a 1.0mb build in US crude stocks amid a 0.1 percentage point predicted decrease in the nation’s refinery utilization rate. Distillate stocks are expected to fall by 0.8mb, whereas gasoline stockpiles are expected to increase by 1.8mb. API petroleum inventories for the same week are due this afternoon at 4:30.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

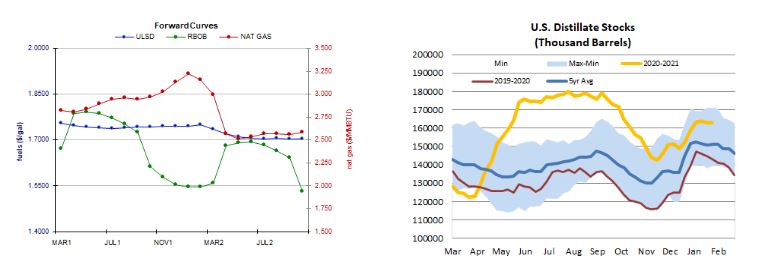

ULSD futures edged up 0.5% today in a thinly-traded upside session, hitting a fresh high of $1.7663 - which becomes nearby resistance, followed by $1.8330. We continue to favor upside chances for now, but again note that both slow stochastics and the RSI are deep into overbought territory. Nearby support at the 9-day ma ($1.6813), followed by $1.6424. RBOB futures also hit a fresh high of $1.6924, but fell back and closed 0.1% weaker, printing a Doji star with long wicks. Overbought slow stochastics have crossed for a sell signal, and the RSI is very much overbought as well. Had we settled in the lower half of the daily range, we might have abandoned the bulls, but for now we'll remain neutral/bullish, seeing $1.7000 and then $1.7500 resistance, with 18-day ma ($1.5906) and then $1.4900 support. WTI futures added 0.7% in an upside session, consistent with our directional bias, and we continue to favor the upside for now. As with products, we note that we are very much overbought. Next resistance at today's $58.62 high, followed by $63.75, while the 9-day ma ($55.32) and then $50.54 are expected to offer support. Lastly, NYMEX natural gas futures fell 1.6% in a downside session, testing the 9-day ma ($2.802) near the lows but settling above it. We adopt a neutral/bearish stance, seeing support at $2.758 and then at the 100-day ma ($2.685), whereas $2.898 and $3.171 remain our nearby resistance levels.