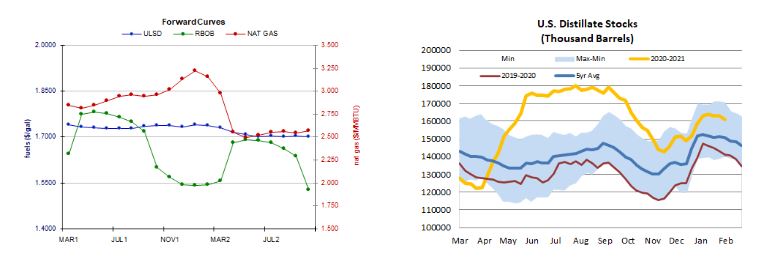

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures turned back south today amid bearish notes from the IEA and OPEC regarding the global oil demand recovery, mostly lower trade in US equities, and strength in the US dollar. The International Energy Agency said that global oil supply continues to outpace demand due to persistent COVID-19 lockdowns and the spread of new virus variants. Also unsupportive, OPEC cut its 2021 oil demand growth forecast by 0.11mb/d to 5.79mb/d, noting that it expects the oil demand to pick up in the second half of the year. In economic news, weekly initial jobless claims came in at 793,000, above expectations at 760,000, but down from 812,000 the prior week. European shares closed flat to higher with the CAC 40 down 0.02%, while the FTSE 100 edged up 0.07% and the DAX added 0.77%. As of this writing, US stock market indexes were trading mixed with the Nasdaq up 0.2%, whereas the S&P 500 was down 0.1% and the Dow had lost 0.4%. Unsupportive for crude oil prices, the US dollar index was up 0.1%.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures fell today amid a weaker two-week heating degree day forecast, a tighter market balance expectation for next week and a bearish weekly storage report from the Energy Information Administration (EIA). The EIA reported a 171bcf withdrawal from underground natural gas storage for the week ended February 5, below forecasts at 181bcf. Total storage levels fell to 2.518tcf, which is 0.4% lower than last year, but 6.4% above the five-year average for the reporting week. The Global Forecast System cut its heating degree day forecast for the next two weeks from 526 to 499, which is closer to but still well above the 30-year average of 395 and last year's 405 HDDs over the same period. Refinitiv analysts now see total US demand of 145.8bcf/d outpacing US supply at 98.3bcf/d next week, implying smaller withdrawals of 47.5bcf/d (compared to yesterday’s forecast at 49.9bcf/d). The latest 1-5 day outlook (EC) sees well below-normal temperatures in the Midwest and the Northeast, with large deviations below normal expected in the central part of the country. The 6-10 forecast also calls for well-below normal temperatures in the Midwest, while mixed temperatures are seen in the Northeast. In the cash market today, prices at the Henry Hub benchmark rose from $3.35 to $3.76/mmBtu, Transco Zone 6 prices in New York jumped from $4.19 to $4.51/mmBtu, and Algonquin citygate prices jumped from $10.85 to $11.50/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures fell 0.9% in a downside session – inconsistent with our bullish bias. Slow stochastics and the RSI are still overbought, while candlesticks are neutral, and the MACD continues to point higher. We are going to stick with bulls for a bit longer, awaiting further bearish confirmation, still seeing nearby resistance at $1.7677 (yesterday’s high), followed by $1.8330, whereas the 9-day ma ($1.7153) and $1.6424 are expected to offer support. RBOB futures gapped lower but rose intraday, still settling 0.2% lower in a downside session – somewhat consistent with our neutral bias which we maintain. We continue to see nearby support at the 18-day ma ($1.6030) and then down at $1.4900, with $1.7000 and $1.7500 seen offering resistance. WTI futures settled 0.7% lower in a downside session today. Slow stochastics and the RSI are still overbought, while candlesticks are neutral, and the MACD is bullish. We are going to stick to our bullish stance for now, awaiting bearish confirmation. Nearby resistance is seen at $58.91 (yesterday’s high) and then up at $63.75, while the 9-day ma ($56.71) and $50.54 are expected to offer support. NYMEX natural gas futures gapped higher but dropped 1.5% in an upside session – consistent with our neutral/bearish stance. Bears took out $2.898 support level, which now becomes nearby resistance, followed by $3.171, whereas $2.758 and the 100-day ma ($2.702) are seen as nearby support levels.