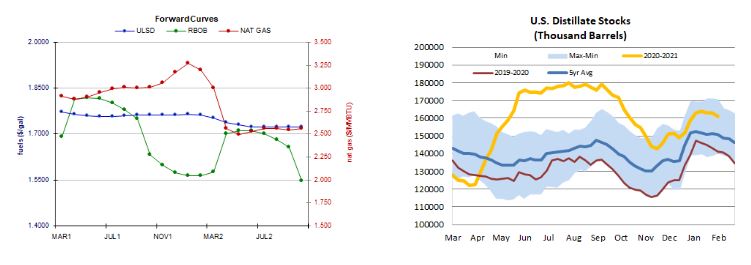

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex resumed its upward march today, with WTI posting gains of 2.1% and led by RBOB futures (up 2.6%), amid flat to higher trade in US and European shares, but despite early strength in the dollar and another weekly rise in the US oil rig count. European shares strengthened today with the DAX up 0.1%, the CAC 40 gaining 0.6% and the FTSE 100 in the UK strengthening 0.9% following encouraging GDP data for December and for the fourth quarter overall. Trade in US shares was more mixed as of this writing, with the Dow down 0.1% but both the S&P 500 and Nasdaq having edged up 0.1%. The preliminary University of Michigan consumer sentiment index for this month was a miss, with a surprise drop to 76.2, whereas a rise to 80.9 had been predicted. The US dollar index had been up by about 0.3% early in the session today, but had come off and was trading near the unchanged mark as of this writing. In unsupportive supply side news, Baker Hughes reported yet another weekly rise in the US oil rig count, of 7 this time to 306. This is, however, still a drop of 372 from the same week last year.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures strengthened today with a drop in the rig count and a tighter US market balance forecast for next week, but despite a downward revision to the heating degree day forecast for the next two weeks. Baker Hughes reported a drop of 2 in the US natural gas rig count this week, but at 90 - compared to 110 last year during the same week. Also supportive, Refinitiv analysts raised their total US demand forecast for next week by 0.4 to 146.2bcf/d, while cutting their supply forecast by 1.2 to 97.1bcf/d, implying withdrawals of 49.1bcf/d. On the other hand, the Global Forecast System sees 474 HDDs over the next two weeks - down from 499 previously and closer to the 30-year average of 391 and last year's 405 HDDs. The near-term outlook remains highly supportive, with large double-digit deviations below normal temperatures expected across a large swathe of the center of the country (ECMWF). Next-day Henry Hub cash prices shot up $2.74 to $6.50/mmBtu, Transco Zone 6 prices in New York climbed $1.36 higher to $5.87/mmBtu, and Algonquin citygate prices strengthened by $1.25 to $12.75/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures opened weaker, testing nearby support at the 9-day ma ($1.7289) at the lows but recovering and hitting a fresh high before settling 1.5% stronger. We stuck with the bulls yesterday, and continue to do so for now, seeing nearby resistance at today's $1.778 high, followed by $1.8330, whereas the 9-day ma ($1.7289) and then $1.6424 remain nearby support. We were neutral regarding RBOB, which also hit a lower low today - but also recovered and hit a fresh high of $1.7006, settling 2.6% stronger. We remain on the sidelines, with an oversold RSI - although slow stochastics are more neutral. Major averages point higher. We see nearby resistance at today's $1.7006 high, followed by $1.7500, whereas the 18-day ma ($1.6115) and then $1.4900 are seen offering support. WTI futures gapped lower and fell further to test nearby 9-day ma support ($57.37) but turned higher and hit a fresh high of $59.82, settling 2.1% higher today. Today's gains were consistent with our upside bias, which we maintain - seeing next resistance at $59.82 and then $63.75, with 9-day ma and then $50.54 support. Lastly, NYMEX natural gas futures added 1.5% today but in a downside session, not too inconsistent with our neutral/bearish view, which we maintain. We see nearby support at $2.898, followed by $3.171, with $2.758 and then 100-day ma ($2.712) support. Slow stochastics, candlesticks, and the RSI are quite neutral, while major averages and the MACD are neutral/bullish.