PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures settled higher today amid production shutdowns in Texas and mostly higher trade in US equities, despite losses in European shares and gains in the US dollar index. Reuters reported that a deep freeze in Texas has left around 4.3 million people without power and has caused about 3.3mb/d of refining capacity (about 18% of national capacity) to shut down. According to Reuters, the following refineries have been shut: Valero Port Arthur (335kb/d), Motiva Port Arthur (607kb/d), Marathon Galveston (585kb/d), Total Port Arthur (225kb/d), Exxon Baytown (560kb/d), Exxon Beaumont (369kb/d), and some units at Citgo Corpus Christi (167kb/d). In European economic news, the German ZEW Survey’s current conditions index came in at -67.2, down from -66.4 in January and below the Econoday consensus at -67.0. On the other hand, the economic sentiment index from ZEW rose from 61.8 to 71.2 this month, while expectations called for a dip to 60.0. The second estimate of fourth quarter GDP for the Eurozone showed a 0.6% quarterly decline (vs -0.7% expected). Despite mostly supportive economic data, European shares closed flat to lower today with the CAC 40 steady, while the FTSE 100 edged down 0.1% and the DAX fell 0.3%. In US news, the Empire State Manufacturing Index jumped from 3.5 to 12.1 this month, beating forecasts at 5.7. As of this writing, US stock market indexes were trading mixed with the Nasdaq down 0.2%, whereas the S&P 500 was up 0.1% and the Dow had added 0.3%. The US dollar index was up 0.1%, which is unsupportive for crude oil prices.

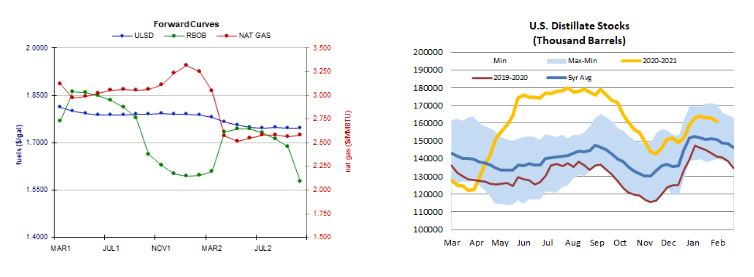

Forward Curves and Stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures rallied today amid power outages in Texas and a looser US market balance expectation for this week, despite a weaker two-week heating degree day forecast. Refinitiv analysts raised their total US demand forecast for the current week by 0.8bcf/d to 147.0bcf/d, while cutting their totally supply forecast by 5.2bcf/d to 91.9bcf/d – implying larger withdrawals of 55.1bcf/d. The market is seen tightening next week, with demand seen falling to 123.2bcf/d, while supply is expected to increase to 92.2bcf/d, implying withdrawals of 31.0bcf/d. The Global Forecast System cut its heating degree day forecast for the next two weeks from 449 to 425, which is closer to but still above both the 30-year average of 377 and last year's 389 HDDs over the same period. The latest 1-5 day forecast based on the European model continues to call for large deviations below-normal temperatures in the central part of the country, while the East Coast is expected to see mostly below-normal temperatures. The 6-10 day outlook (EC) is less supportive as mixed temperatures are expected in both the Midwest and the Northeast. In the cash market today, prices at the Henry Hub benchmark fell from $6.50 to $6.12/mmBtu, Algonquin citygate prices dropped from $12.75 to $11.25/mmBtu, and Transco Zone 6 prices in New York fell from $5.87 to $5.73/mmBtu. According to a Reuters poll of analysts, estimates for the weekly EIA petroleum inventory report for the week ended February 12 call for a 2.2mb draw from US crude stocks and a 0.2 percentage point predicted decrease in the nation’s refinery utilization rate. Distillate stocks are expected to fall by 1.8mb, whereas gasoline stockpiles are expected to increase by 1.4mb. API petroleum inventories for the same week are due tomorrow at 4:30, due to the holiday on Monday.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures climbed another 2.4% higher today, consistent with our upside bias, in a heavily-traded upside session (higher high, higher low), hitting fresh highs not seen since early last year. Slow stochastics and the RSI remain overbought, while other indicators point higher. We see nearby resistance at $1.8330 and then $1.9000, while the 9-day ma ($1.7441) and then $1.6424 remain nearby support. RBOB futures led the complex higher, jumping 4.8% higher and also hitting new levels not seen since early 2021. We continue to favor upside chances, with resistance at today's $1.7927 high, followed by $1.8500, with support at the 18-day ma ($1.6241) and then down at $1.4900. WTI futures posted slimmer gains of 1.0% today, printing a Doji star. Slow stochastics and the RSI are both overcooked. We'll wait for a clearer sign that the trend has ended before abandoning the bulls. Higher chances for higher prices, with next resistance at today's $60.95 high (followed by $63.75), whereas $59.50 and then the 9-day ma ($57.95) are our nearby support levels. Natural gas futures trade today was inconsistent with our neutral/bearish bias, as we gapped sharply higher and then strengthened further, closing up 7.5% in an upside session. The MACD points higher, as do the major averages, while the RSI and slow stochastics are more neutral. We are back on the sidelines, looking to see if bulls can follow through on today's price action.