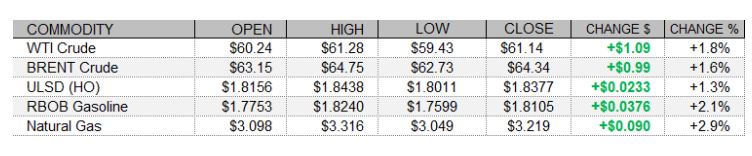

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The rally continued today, with oil production and refinery outages continuing in Texas, as well as generally encouraging economic data releases, despite mostly weaker trade in equities and strength in the US dollar. The FTSE 100 fell 0.6% today, the CAC 40 shed 0.4%, and the DAX dropped 1.1% lower. North American economic data releases were generally encouraging. Canadian consumer price inflation was stronger than expected last month, with the CPI up 0.6%, and US producer price inflation was also stronger than expected at 1.3%. US industrial production growth of 0.9% last month beat the 0.5% forecast, and the NAHB Housing Market Index saw a surprise increase to 84 this month. Finally, today's headline item was a beat, with US retail sales gaining 5.3% last month, well above expectations at 1.1%. The Dow was up 0.1% as of this writing, but the S&P 500 was off 0.3% and the Nasdaq was down 0.9%. Also unsupportive for oil, the US dollar index was rallying 0.5%. In supportive news, Reuters reports that Wood Mackenzie estimates some 1mb/d of crude oil production has been shut in Texas, and that it could take weeks for a complete restoration of output. Additionally, almost 4mb/d of refining capacity has been knocked out by the polar vortex event, per Reuters calculations.

NATURAL GAS | WEATHER | INVENTORIES

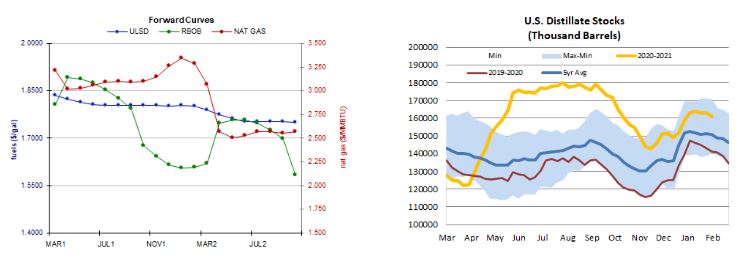

Natural gas futures strengthened once again today, with a tighter picture of next week's US market balance, despite a drop in the two-week heating degree day forecast. Refinitiv analysts cut their total US supply forecast for next week by 3.0 to 89.2bcf/d, outpacing a 1.0bcf/d cut to the demand forecast to 122.2bcf/d, implying larger withdrawals from storage of 33.0bcf/d. For the next two weeks overall, the Global Forecast System sees 401 HDDs, down from 425 previously and closer to last year's 405 HDDs as well as the 30-year average of 374. The 1-5 day outlook (ECMWF) continues to call for below-normal temperatures across the country and double-digit deviations below normal for the central portion of the country near the Mississippi. The 6-10 day forecast, however, calls for well-above-normal temperatures in parts of the Midwest and mixed but mostly above-normal temperatures for much of the East Coast. The EIA is due to release its natural gas storage report for the week ended February 12 tomorrow, and is expected to show a 252bcf withdrawal, well above last year's 141bcf drop and the 142bcf five-year average. Petroleum inventories for the same week are also due tomorrow, a day late due to the holiday on Monday. According to a Reuters poll, crude stocks are seen falling by 2.4mb despite a 0.2pp predicted downtick in the refinery utilization rate, to 82.8%. Distillate stocks are seen drawing down 1.6mb, while gasoline stocks are expected to build 1.4mb.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures added 1.3% in an upside session (higher high, higher low) – consistent with our bullish bias which we continue to maintain. Bulls took out nearby $1.8330 resistance, which now becomes nearby support, followed by the 9-day ma ($1.7606), while $1.9000 and $1.9509 are expected to offer resistance. RBOB futures rose 2.1% in an upside session – also consistent with our upside bias. We remain bullish, seeing nearby resistance at $1.8240 (today’s high) and then at $1.8500, while the 18-day ma ($1.6387) and $1.4900 are seen as nearby support levels. WTI futures, where we were bullish, settled 1.8% higher in an upside session. We continue to favor upside chances, still seeing nearby support at $59.50, followed by the 9-day ma ($58.55), with $61.28 (today’s high) and $63.75 expected to offer resistance. NYMEX natural gas futures gained 2.9% in an upside session – inconsistent with our neutral bias. Slow stochastics and the RSI point higher, along with the candlesticks and the MACD, so we are going to side with the bulls now. Nearby resistance is seen at $3.316 (today’s high) and then up at the $3.500 mark, while $2.898 and $2.758 are seen offering support.