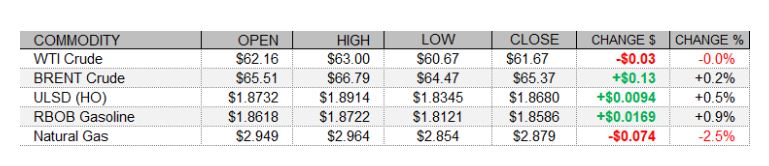

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures settled flat to higher today amid a bullish revision to Morgan Stanley's oil price forecast and indications that the return of US shale oil production in Texas could take two weeks or more, despite losses in US equities and strength in the US dollar. Morgan Stanley sees Brent crude prices rising to $70/bbl in the third quarter, and revised up its fourth-quarter price forecast from $60/bbl to $65/bbl, with a decline in the number of new coronavirus cases globally, a bottoming out of mobility statistics, and recovered refining activity in non-OECD countries to pre-pandemic levels. In European economic news, consumer price inflation in the Eurozone matched expectations in January, with the HICP up 0.2% as expected. The FTSE 100 and the CAC 40 closed 0.2% higher, while the DAX lost 0.6%. In US news, the S&P CoreLogic Case-Shiller Home Price Index rose 1.3% in December, above the Econoday consensus at 1.0%. Also supportive, the Conference Board's Consumer Confidence Index rose from a downwardly-revised 88.9 to 91.3 this month, beating expectations at 90.0. As of this writing, US stock market indexes were seeing losses of between 0.3% (Dow) and 1.7% (Nasdaq). Also unsupportive for crude oil prices, the US dollar index was up 0.15%, after spending three sessions lower.

NATURAL GAS | WEATHER | INVENTORIES

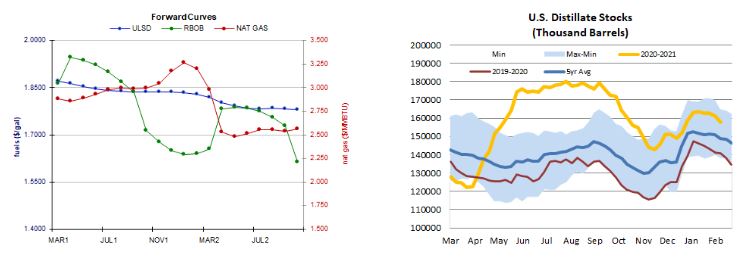

Natural gas futures extended their losses today amid a moderating temperature outlook, a weaker two-week heating degree day forecast, and a looser US market balance expectation for next week. The Global Forecast System cut its heating degree day forecast for the next two weeks from 301 to 296, which is well below both the 30-year average of 351 and last year's 326 HDDs over the same period. The latest 1-5 day outlook (EC) calls for above-normal temperatures across the eastern half of the country. The 6-10 day forecast sees mixed temperatures in the Midwest, while above-normal temperatures are expected in the Northeast. In the cash market today, prices at the Henry Hub benchmark fell from $4.96 to $3.16/mmBtu, Algonquin citygate prices dropped from $6.64 to $2.69/mmBtu, and Transco Zone 6 prices in New York dropped from $6.82 to $4.16/mmBtu. Refinitiv analysts now see total US demand of 109.1bcf/d outpacing US supply at 97.8bcf/d next week, implying smaller withdrawals of 11.3bcf/d (compared to yesterday’s forecast at 18.7bcf/d). According to a Reuters poll of analysts, estimates for the weekly EIA petroleum inventory report for the week ended February 19 call for a 5.2mb drop in US crude stocks despite a 6.7 percentage point predicted decrease in the nation’s refinery utilization rate. Distillate stocks are expected to fall by 3.7mb and gasoline stockpiles are expected to drop by 3.1mb. API petroleum inventories for the same week are due this afternoon at 4:30.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures gapped higher and went on to hit a fresh high of $1.8914 and to also threaten $1.8330 support at the lows, printing a Doji star with very long wicks - indicating ambivalence. Reinforcing this ambivalence, there was strong volume behind today's trade. The MACD and major averages point higher, while the RSI and slow stochastics remain bearish. We remain on the sidelines, still seeing nearby support at $1.8330 and then down at the 9-day ma ($1.8130), with resistance at today's $1.8914 high and then up at $1.9509. RBOB futures also gapped higher and then fell, hitting a low point at about the middle of yesterday's trading range, but recovered to close near the open of today's upside session. Additionally, we saw a fresh high of $1.8722, which becomes nearby resistance, followed by $1.9000. We see support at $1.6956, reinforced currently by the 18-day ma. Slow stochastics and the RSI are overbought, while other indicators point higher - but today's candlestick pattern can precede reversals. We remain neutral/bullish for now. WTI futures gapped higher and hit a new high of $63.00 in today's upside session, printing a Doji star. Slow stochastics look set to re-cross in neutral territory, while the RSI remains overbought. Major averages and the MACD point higher. We remain neutral, and today's change of less than 0.1% is consistent with that view. We see nearby resistance at the new $63.00 high, followed by $66.85, with 9-day ma ($60.08) and then $57.21 support. Finally, natural gas futures continued lower today, taking out $2.898 support along with the 18-day ma ($2.903) in the process. We side with the bears, given bearish slow stochastics, RSI, and candlesticks, and a bearish cross in the MACD. Next support at $2.758 and then at $2.403, with $2.898 and then $3.316 (recent high) resistance.