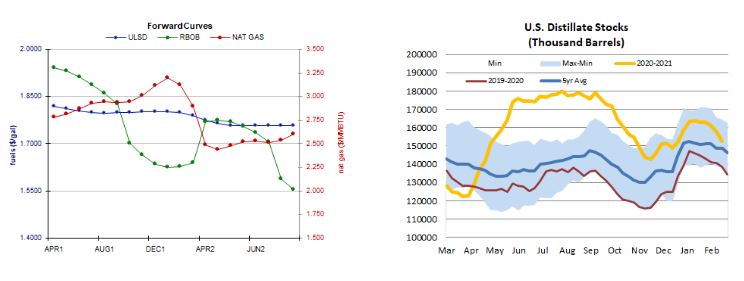

PETROLEUM COMPLEX (WTI | BRENT | ULSD/Heating Oil | RBOB)

Petroleum futures spent most of the early part of the session near and to the north of the unchanged mark, but came off later in the session. This third session lower for Brent and products (and second session lower for WTI) came despite encouraging economic data releases and strength in equities, but further strength in the US dollar was unsupportive. As of this writing, the US dollar index was up 0.25% and near its highest levels since February 8. On the other hand, the DAX, CAC 40, and FTSE 100 all saw gains of 1.6% today following encouraging Eurozone, German, and UK manufacturing data. US shares were rallying over two percent as of this writing, with the Dow up 2.1%, the S&P 500 having gained 2.3%, and the Nasdaq up 2.5%. Both the final Markit Manufacturing PMI (58.6) for February and the ISM Manufacturing PMI (60.8) for the same month for the US beat expectations. Additionally, January construction spending growth of 1.7% was well above the 0.8% expectation and came with a slight upward revision to December spending. Also supportive was the emergency use approval for Johnson & Johnson's one-shot coronavirus vaccine, and the passage by the House of the $1.9tn stimulus bill, which now goes to the Senate.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX saw see-saw trade about the unchanged mark today, despite largely supportive developments. The Global Forecast System raised its two-week Heating Degree Day forecast from 257 to 279, above last year's 256 HDDs during the same period - but below the 30-year average of 328. Taking a regional perspective, the near-term outlook is supportive for the East Coast but unsupportive for the Midwest, as both the 1-5 day and 6-10 day ECMWF outlooks call for well-above-normal temperatures in the Midwest, but below-normal temperatures for the East Coast. Cash natural gas prices were mixed, with Henry Hub down by 6 cents to $2.66/mmBtu, but with a 2-cent rise in Transco Zone 6 prices to $2.38/mmBtu and a 70-cent jump in Algonquin citygate pricing to $2.60/mmBtu. Refinitiv analysts see total US demand of 111.3bcf/d outpacing total US supply of 98.7bcf/d by 12.6bcf/d this week, but expect the market balance to loosen next week, with 102.9bcf/d demand and 98.6bcf/d demand implying withdrawals of just 4.3bcf/d.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX HO futures fell 1.3% today in an average-volume downside session, with bears following through on Friday's price action and taking out support at both the 9-day ma and at $1.8330. These become our nearby resistance levels, and we look to the 18-day ma ($1.8008) for nearby support - this had been S2 and also held up to a test at the lows today. After the 18-day, we would look to the $1.7000 psychological level. Slow stochastics, the RSI, and candlesticks all point lower, and the MACD has crossed and gone from bullish to neutral. RBOB futures gapped sharply higher with the front switch, something we failed to account for in setting resistance and support levels in our commentary on Friday. We settled down 0.4%, but well above the highs from the previous three sessions for the old front month, and setting fresh highs for a front month. Slow stochastics and the RSI are overbought, and the price action can often serve to close the front switch gap. We favor downside chances, seeing support at $1.9050 and then down at the 18-day ma ($1.7654), whereas $2.000 and then $2.1108 are seen offering resistance. As with HO, we received bearish confirmation in WTI trade today and favor further downside movement chances, looking to $59.47 and then $57.21 for support, and to the 9-day ma ($61.43, taken out today) and then $63.81 resistance. Slow stochastics and the RSI are bearish, and the MACD has crossed, becoming neutral. Natural gas futures edged up 0.2% in an upside session. Oversold slow stochastics have crossed for a buy signal, but the RSI is much more neutral (46.5), and so are the candlesticks from the past three sessions, with trade hovering just north of $2.758 support (followed by $2.403). We'll fall back to the sidelines, looking to $2.898 and then $3.316 for resistance.