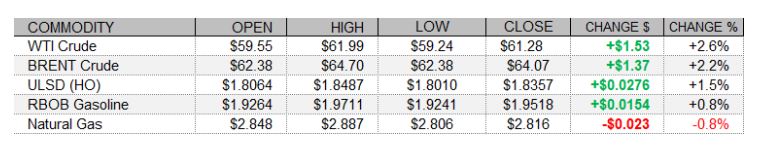

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Brent crude oil and refined products futures snapped a four-session sell-off today amid bullish US weekly product inventories from the EIA, strength in European shares, and expectations that OPEC+ would roll rather than relax its current output policy, despite strength in the US dollar and mixed but mostly lower trade in US shares following a miss in the ADP jobs report. The payroll processor reported a rise of 117,000 in private payrolls last month, well below consensus at 165,000. A 21,000 upward revision to January payrolls was insufficient to make up for the miss. Also a miss was the US ISM Services Index for last month, which saw an unexpected fall from 58.7 to 55.3. Weekly US crude stock data from EIA were very bearish, as the agency reported a record weekly 21.6mb build. On the other hand, product stocks saw much sharper than expected declines are refinery utilization rates saw further surprise drop on the Gulf Coast.

NATURAL GAS | WEATHER | INVENTORIES

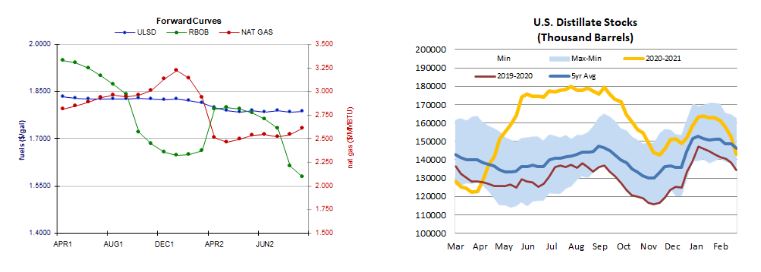

Natural gas futures on NYMEX strengthened today with an upgrade to the two-week heating degree day forecast and a tighter US market balance expectation for next week. Refinitiv analysts revised their total US demand forecast for next week up by 2.8 to 105.0bcf/d, while cutting their supply forecast by 1.5 to 98.6bcf/d, implying 6.4bcf/d withdrawals from storage - compared to 2.1bcf/d previously. Also supportive, the Global Forecast System sees 295 HDDs over the next two weeks, up from 279 previously, above last year's 256 HDDs and closer to the 30-year average of 320. The latest 1-5 day ECMWF outlook sees much warmer than normal temperatures in the Midwest, but below-normal temperatures on the East Coast, particularly in Vermont. Cash natural gas prices made mixed moves, with benchmark Henry Hub prices up 17 cents to $2.87/mmBtu, but Transco Zone 6 prices at the New York citygate fell 11 cents to $2.73/mmBtu and Algonquin citygate prices tumbled $2.46 lower to $4.04/mmBtu. The 6-10 day ECMWF outlook calls for above-normal temperatures across the eastern two-thirds of the country, especially in the Midwest. The weekly EIA storage report is due tomorrow, expected by analysts (Reuters poll) to show a 136bcf withdrawal, topping last year's 119bcf drop and the 81bcf five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures added 1.5% in an average-volume upside session today, not so consistent with our bearish bias. We saw a Doji star shaped candlestick in yesterday’s session, which usually indicates a reversal which we saw today. Slow stochastics are still bearish, while the RSI and moving averages are bullish, and the MACD and candlesticks are neutral. We are going to fall onto the sidelines now, seeing nearby support at $1.8330 (taken out today) and then down at the 18-day ma ($1.8151), whereas the 9-day ($1.8542) and $1.9193 (recent high) are expected to offer resistance. RBOB futures, where we were also bearish, gapped lower but rose intraday to settle 0.8% higher in an upside session. Slow stochastics are bearish and the RSI is still overbought, while candlesticks are neutral and the MACD is bullish. We are going to continue to favor downside chances for a bit longer, seeing nearby support at $1.9050 and then down at the 18-day ma ($1.7987), while $2.0000 and $2.1108 are seen offering nearby resistance. WTI futures rose 2.6% in an outside session (higher high, lower low) with bulls taking out the 18-day ma ($60.20) and testing but failing to take out the 9-day ma ($61.37). We continue to see nearby resistance at the 9-day ma, followed by $63.81, with $59.47 and $57.21 seen as nearby support levels. Stochastics are bearish, while the RSI, the MACD, and candlesticks are neutral. We remain bearish for now, awaiting further developments. Lastly, NYMEX natural gas futures gapped higher but fell intraday to settle 0.8% lower in an upside session – consistent with our neutral bias. We remain neutral, looking at $2.898 and then at $3.316 for resistance, whereas $2.758 and $2.403 are our nearby support levels.