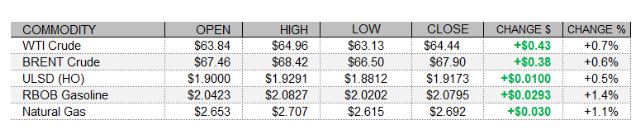

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex saw see-saw trade relatively close to the unchanged mark today, settling higher. Weekly EIA inventories were supportive of wider crack spreads - particularly gasoline - as the agency reported a much larger than predicted build in crude stocks, but larger than predicted declines in distillate and, especially, gasoline inventories. US oil production continued to return in the week ended March 5, as did Gulf Coast refining operations, following the Texas freeze. See our DOE Report for more. Whereas EIA crude stock data were bearish, trade in global shares today was supportive for crude. European shares closed flat to higher with the FTSE 100 off 0.07%, the DAX gaining 0.71%, and the CAC 40 rallying 1.11%. As of this writing, US stock market indexes were seeing gains as well, with the Nasdaq up 0.2%, the S&P 500 up 0.8%, and the Dow strengthening 1.4%. Meanwhile, the US dollar index was fairly steady, just south of the unchanged mark and slightly supportive for crude. The Bank of Canada kept monetary policy settings unchanged this month, consistent with market expectations. US consumer price inflation matched expectations last month, with the CPI up 0.4% m/m. Core price growth of 1.3% year-on-year was just under the 1.4% expectation and well below the 2.0% symmetric FOMC target.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures also saw see-saw trade today, settling slightly higher. In unsupportive news, the Global Forecast System once again trimmed its two-week HDD forecast, by 23 to 236, which is now below last year's 246 HDDs and also the 30-year average for the period of 291. The 1-5 day ECMWF outlook remains unsupportive, as well above normal temperatures are expected in the Midwest, South, and on the East Coast. The 6-10 day outlook is more supportive, with below-normal temperatures expected in the Northeast, and mixed temperatures in the Midwest. Refinitiv analysts raised their total US demand forecast for next week by 0.3bcf/d to 103.1bcf/d, outpacing a 0.20bcf/d upward revision to their supply forecast to 99.6bcf/d, implying slightly larger 3.5bcf/d withdrawals. Next-day Henry Hub cash natural gas prices weakened by 5 cents to $2.62/mmBtu, Transco Zone 6 prices at the New York citygate fell 12 cents to $2.24/mmBtu, and Algonquin citygate prices shed 6 cents, slipping down to $2.70/mmBtu. The EIA is due to release its weekly natural gas storage report tomorrow, expected to show a 73bcf withdrawal for the week ended March 5. This would be close to last year's 72bcf withdrawal but smaller than the 89bcf five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

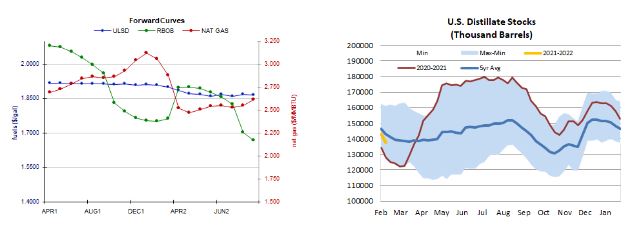

ULSD futures rose 0.5% today but did so in a downside session – somewhat consistent with our bullish bias. The RSI is neutral now, along with candlesticks and the MACD, while slow stochastics point lower. We are going to stick to our bullish bias for a bit longer, awaiting further developments, still seeing nearby resistance at $1.9695 and then up at $2.0000, while the 9-day ma ($1.8769) and $1.8330 are expected to offer support. RBOB futures, where we were also bullish, gapped lower but rose intraday to settle 1.4% higher in a downside session. We are going to stick with the bulls for now, still looking at $2.1119 (recent high) and $2.1904 for resistance, while $2.0000 and the 18-day ma ($1.9064) are seen as nearby support levels. Similar to products, WTI futures added 0.7% in a downside session today. Slow stochastics point lower, while the RSI, the MACD, and candlesticks are all neutral. We are going to continue to favor upside chances for now. We continue to see nearby support at $63.75, followed by $59.67, with $66.85 and $73.29 expected to offer resistance. Finally, NYMEX natural gas futures rebounded today and rose 1.1% in an outside session – not so consistent with our bearish bias. Slow stochastics crossed bullishly and are leaving oversold territory and the RSI points higher, while the MACD and candlesticks are neutral. We are going to fall back onto the sidelines now. Nearby resistance is seen at $2.758 and then up at $2.898, while $2.403 and $2.000 remain our nearby support levels.