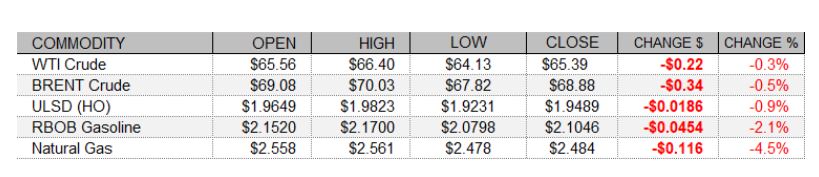

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures fell for a second session as the US dollar index rose for a second session as well, with weakness in European shares also likely weighing on the crude price action, even as US shares strengthened amid mostly encouraging North American economic data releases. While Canadian housing starts for February were a miss, coming in at a 245,922 annualized rate and short of consensus at 248,000, Canadian manufacturing sales growth of 3.1% in January beat forecasts at 2.5%. In US news, the Empire State Manufacturing index rose from 12.1 last month to 17.4 this month, topping expectations at 14.8. As of this writing, US stock market indexes were seeing modest gains, with both the S&P 500 and the Dow up 0.1%, while the Nasdaq had added 0.3%. On the other hand, the US dollar index was up 0.16% and European shares closed lower. Both the FTSE 100 and CAC 40 shed 0.2%, while the DAX lost 0.3% today.

NATURAL GAS | WEATHER | INVENTORIES

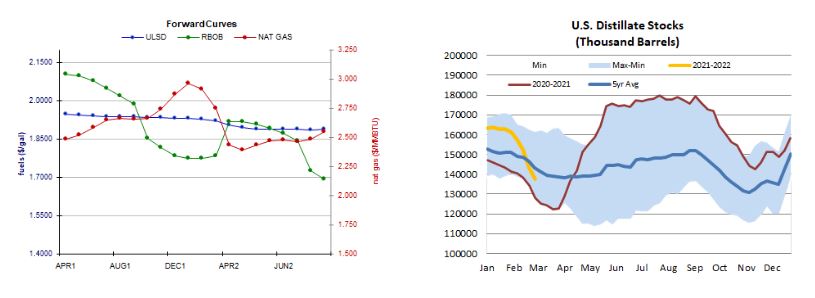

Natural gas futures slid for a third session today with a weaker degree forecast and loosening projected US market balance. The Global Forecast System cut its two-week HDD forecast from 247 to 227, well below the 30-year average of 270 and also below last year's 241 HDDs during the same period. Refinitiv analysts see total US demand of 103.1bcf/d outpacing total US supply of 98.7bcf/d this week, implying 4.4bcf/d withdrawals, but see demand falling by 4.1 to 99.0bcf/d net week, while supply rises by 0.2 to 98.9bcf/d, suggesting withdrawals of only 0.1bcf/d. The latest 1-5 day ECMWF forecast calls for mostly above-normal temperatures in the Midwest, but below-normal temperatures in the Northeast. Algonquin citygate next-day cash natural gas prices fell by 6 cents to $2.25/mmBtu, but Transco Zone 6 prices in New York jumped 32 cents higher to $2.37/mmBtu. Prices at Henry Hub slipped 5 cents lower to $2.65/mmBtu. The 6-10 day ECMWF outlook is unsupportive, calling for well-above-normal temperatures in the Midwest and above-normal temperatures in the Northeast as well.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures slipped 0.9% lower today in a relatively thinly-traded upside session (higher high along with the lower low). Bears tested nearby 9-day ma support ($1.9202) at the lows, but failed, and we settled well off of the intraday lows and in the top half of the daily range. Accordingly, we'll keep to our upside bias for now, even though we note that slow stochastics, the MACD, and candlesticks are all now neutral. Major averages and the ADX point higher, while the RSI is bearish. RBOB futures fell 2.1% today but hit a fresh multi-year high and settled well off of the lows. Slow stochastics and the RSI are overbought, however. We'll remain neutral/bullish for now, seeing support at the $2.0000 mark, followed by the 18-day ma at $1.9684, whereas the new $2.1700 high and then $2.1904 are our nearby resistance levels. WTI futures edged down 0.3% in an outside session, printing a Doji star. We remain neutral/bullish, looking to $66.85 and then $73.29 for resistance, whereas $63.75 and $59.67 remain nearby support. We sided with natural gas bears on Friday, and were rewarded with a fairly wide gap lower over the weekend and a 4.5% drop. We remain bearish, noting that both the slow stochastics and the RSI have room to fall, while candlesticks and the MACD point lower, and the major averages are shifting from neutral to bearish as the price action pulls the short averages down. We expect support at $2.403 and then at $2.000, while $2.758 and $2.898 remain nearby resistance.