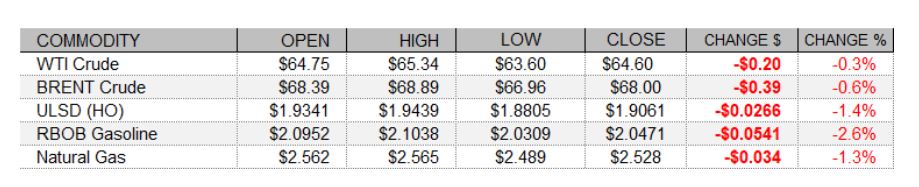

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures fell for a fourth consecutive session and products weakened for a third today, as the US dollar index saw modest gains for a fourth day and the EIA provided unsupportive weekly US crude oil and products stock data. The agency reported a larger than expected build in commercial crude oil inventories and small - but surprise and counter-seasonal - builds in both distillate and gasoline stockpiles. Crack spreads narrowed today, as RBOB and ULSD (HO) futures fell faster than WTI crude futures, consistent with the data. European shares closed mixed following neutral Eurozone consumer price inflation data. The FTSE 100 fell 0.6%, but the CAC 40 was steady, and the DAX gained 0.3%. In US news, housing starts slowed from a 1.584m annualized pace in January to 1.421m last month, short of expectations at 1.570m. Permits were also a miss, slowing from 1.886m to 1.682m, below consensus at 1.750m. The Federal Open Market Committee kept its Fed funds rate target a 0-0.25%, as widely expected. While it stated that "indicators of economic activity and employment have turned up recently," it reaffirmed its commitment to allowing inflation to run "moderately" over 2% for some time in order to strongly anchor long-term inflation expectations at 2%. Purchases of $80bn/mo of Treasuries and $40bn/mo of agency MBS continue. US shares were mixed as of this writing, with the Nasdaq down 0.4%, the S&P 500 about flat, while the Dow was up 0.6%.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX turned back south today with relatively warm temperatures on tap and a looser US market balance forecast for next week. The latest 1-5 day ECMWF outlook calls for warmer than normal temperatures in the Midwest, particularly in the northern tier states, as well as for much of the Northeast. Next-day cash natural gas prices fell, with Transco Zone 6 (NY) prices down 9 cents to $2.26/mmBtu, Algonquin citygate prices falling $1.45 to $2.51/mmBtu, and benchmark Henry Hub prices shedding 8 cents and slipping down to $2.50/mmBtu. The 6-10 day and 11-15 day ECMWF outlooks call for above-normal temperatures across the eastern half of the country, and Refinitiv analysts see total US demand falling by 0.6 to 99.5bcf/d next week (while supply falls by just 0.1 to 98.8bcf/d). Consistent with this, the Global Forecast System sees 220 HDDs over the next two weeks, down from 222 previously and well below both last year's 241 HDDs and the 262-HDD 30-year average. The EIA is due to report US natural gas storage levels for the week ended March 12 tomorrow morning, and analysts polled by Reuters expect to see a 30bcf withdrawal in the report. This would be larger than last year's 15bcf drop, but smaller than the 59bcf five-year average.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

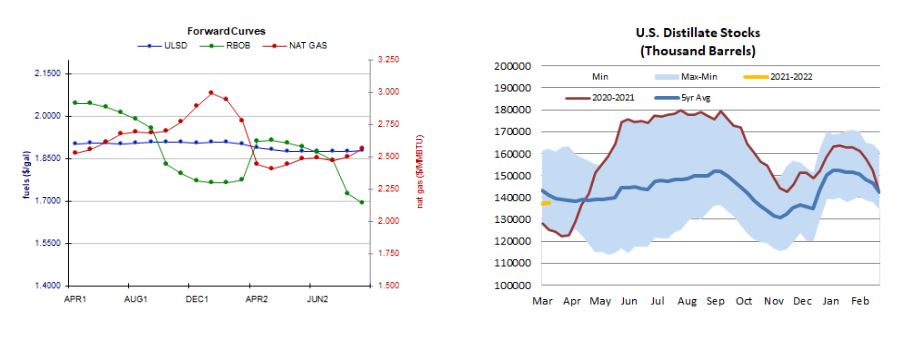

ULSD futures fell 1.4% in a downside session with bears taking out 9-day ma ($1.9327) support and testing but failing to take out the 18-day ma ($1.8973). Slow stochastics and the RSI point lower, along with candlesticks, while the MACD is neutral. We are going to side with the bears now, seeing nearby support at the 18-day ma and then down at $1.8330, while the 9-day ma and $1.9695 are expected to offer resistance. RBOB futures dropped 2.6% in a downside session – inconsistent with our neutral/bullish bias. Bears took out the 9-day ma ($2.0873). Slow stochastics, the RSI, and candlesticks are bearish, while the MACD is neutral now, and we are going to take a neutral/bearish stance now. Nearby support is seen at $2.0000 and then at the 18-day ma ($1.9989), with $2.1700 (recent high) and $2.1904 expected to offer resistance. WTI futures edged down 0.3% in a downside session – somewhat consistent with our neutral view which we maintain. Slow stochastics, the RSI, and the MACD are all quite neutral. We continue to see nearby resistance at $66.85 and then up at $73.29, whereas $63.75 (tested today) and $59.67 are seen offering support. NYMEX natural gas futures, where we were bearish, lost 1.3% in an inside session today. We are going to stick to our downside bias for now, still seeing nearby support at $2.403 and then down at $2.000, while $2.758 and $2.898 remain our resistance levels.