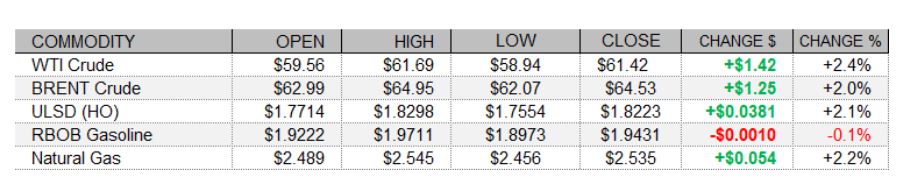

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures saw volatile, see-saw trade today, with crude futures looking set to fall for a sixth session (and product for a fifth) in early going, but with crude futures turning higher to see gains of over two percent. The gasoline crack narrowed further today, as RBOB futures lagged the rest of the complex. Trade in European shares and movements in the US dollar index today were unsupportive. The FTSE 100 fell 0.9%, and both the DAX and CAC 40 dropped 1.10%. The US dollar index rallied to its strongest levels since March 10 today, but came off and was just north of the unchanged mark as of this writing. Meanwhile, trade in US equities was mostly supportive. Although the Dow was down slightly, the S&P 500 was seeing modest strength and the Nasdaq was up 1.0%. Also supportive today was news that Houthi forces in Yemen claimed to have launched another attack at a Saudi Aramco facility in Riyadh, using six drones. Additionally, investment bank Goldman Sachs made an upward revision to its oil price forecast for the year on stronger global oil demand expectations due to coronavirus vaccinations. European and British regulators have said that benefits of the AstraZeneca vaccine outweigh the risks, and countries are working to resume distribution.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX strengthened today, after two sessions lower, with a tighter US market balance expectation for next week and a slight upward revision to the two-week heating degree day outlook. Refinitiv analysts raised their total US demand forecast for next week by 0.9 to 100.9bcf/d, outpacing a 0.2bcf/d upward revision to the supply forecast (to 98.8bcf/d). Also supportive, the Global Forecast System sees 221 HDDs over the next two weeks, up from 217 previously, but still well below both the 241 HDDs seen last year and the 254-HDD 30-year average. In neutral news today, Baker Hughes reported a steady US natural gas rig count, at 72. The latest 1-5 day ECMWF outlook calls for much warmer than normal temperatures in the Midwest and warmer than normal temperatures for much of the East Coast. Next-day cash natural gas prices in New York and at the Algonquin citygate strengthened nevertheless, with Transco Zone 6 prices up 14 cents to $2.41/mmBtu and Algonquin prices jumping 54 cents higher to $3.30/mmBtu. Benchmark Henry Hub prices, on the other hand, fell back 15 cents to $2.45/mmBtu. The 6-10 day ECMWF outlook calls for above-normal temperatures across the eastern half of the country, with particularly large deviations above normal in the Northeast.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures took a trip south early on to test 50-day ma support ($1.7551), failing, and recovering to settle below nearby $1.8330 resistance, in the upper portion of the daily range. We saw a higher low and a lower high, making it an inside session. This may be the retracement we mentioned could follow yesterday's sharp sell-off. We continue to favor downside chances, seeing as neither the RSI nor slow stochastics are oversold, and as the latter points lower along with the ADX. We see support at the aforementioned 50-day ma, followed by $1.7000, whereas $1.8330 and the then 9-day ma ($1.9052) should offer nearby resistance. RBOB futures edged down 0.1% today in an inside session. Slow stochastics are approaching oversold territory but have yet to reach it, while the RSI is very much in neutral territory at 52.0. We remain bearish, seeing $1.8973 and then 50-day ma ($1.7666) support, while the 18-day ma ($2.0093) and then $2.1700 are expected to offer resistance. WTI futures gapped lower, but recovered and gained 2.4% in an inside session. We settled above $59.67 support (followed by $57.21), and also below $63.75 and $66.68 resistance. We remain bearish, for similar rationale as with refined products. Natural gas futures gapped higher, but tested the 200-day ma at the lows ($2.451), before turning higher and gaining 2.2% today. Slow stochastics are looking bullish, while the RSI is neutral. The MACD is bearish, and major averages are weakening. We'll take neutral/bearish stance, awaiting further developments.